POLICY STATEMENT 037 BY THE INDEPENDENT MEDIA AND POLICY INITIATIVE (IMPI)

IN DEFENCE OF PRESIDENT TINUBU’S DEBTS-FOR-INFRASTRUCTURE POLICY

The nation’s policy space is once again inundated with claustrophobic imputations by politically minded individuals and advocacy groups that stridently demonise the federal administration’s infrastructure policy debts, with a devious objective to disorient the masses against the administration.

Our review of all imputations made in this regard points to a fallacy of generalisation, lacking an alternative workable solution to the historical limitations inherent in Nigeria’s infrastructure deficit and the consequential unproductive impact on the nation’s economy and development.

Infrastructure development, in the context of this Policy Statement, encompasses the construction and maintenance of physical structures such as roads, bridges, power supply, transportation systems, and other enabling facilities that facilitate economic activity and improve the quality of life for citizens.

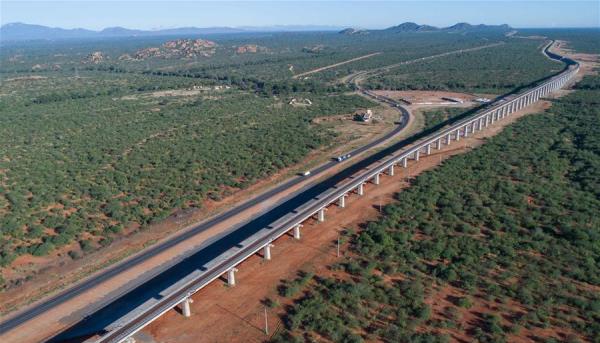

Nigeria’s infrastructure challenges are vast. Road networks, crucial for trade and mobility, span around 195,000 kilometres. Yet, over 70 per cent of these roads are in poor condition, driving up transportation costs, delaying deliveries, and limiting access to markets, especially for small businesses and farmers.

Nigeria’s rail infrastructure is also limited. Despite recent investments, the country has only 3,500 kilometres of operational tracks, insufficient for a population exceeding 220 million. Installed power capacity is 12,500 MW, but actual operational output often averages only 4,000 MW, leaving Nigeria’s per capita electricity consumption at just 144 kWh annually, far below the global average of 3,131 kWh. Businesses spend an estimated $29 billion annually on backup energy sources, including diesel generators. This infrastructural insufficiency was attributed to the exit of companies such as GSK and P&G, among others, over the years.

*Valuation of Nigeria’s Infrastructure Deficit*

Nigeria’s productivity and standard of living have been ascribed to the inadequacy of infrastructure over the years. While there is a seeming consensus on this assertion, there have been diverse estimates of the true value of the country’s infrastructure deficit.

The World Bank, which categorises Nigeria as a middle-income economy, estimated the Nation’s total infrastructure stock to be approximately 30% to 35% of its Gross Domestic Product (GDP). This ratio falls well short of the World Bank’s 70% benchmark for middle-income economies. Thus, it is projected that Nigeria will need an accumulated investment of up to $3 trillion over 30 years to bridge the infrastructure gap.

The African Development Bank (AfDB), on the other hand, estimated the value of the country’s infrastructure shortfall at $2.3 trillion, $700 billion lower than the World Bank’s estimate. According to its erstwhile President, Dr Akinwunmi Adesina, Nigeria needs $15 billion in annual investment over 20 years to bridge its infrastructure gap.

The International Finance Corporation (IFC), on its part, estimated a lower figure of $2 trillion over 20 years to bridge it. Still, KPMG, the global audit firm, estimated a much lower annual infrastructure spending of $14.2 billion over 10 years, totalling a sum of $142 billion to close the country’s huge infrastructure gap.

To establish which of the estimates can be realised in Nigeria’s perennially constricted revenue-generation circumstances, we put the different infrastructure deficit estimates to the test of probable outcomes, which determine the likelihood of specific results from a random event or experiment, often calculated as the ratio of favourable outcomes to total possible outcomes.

Among all the estimates, KPMG’s $142 billion estimate aligned more closely with the Nigerian situation, with a probable outcome indicating that spending $14.2 billion annually over 10 years (a total of $142 billion) is a key target to bridge Nigeria’s infrastructure gap. Accordingly, sustained investment at this level, particularly in transportation, power, and digital infrastructure, will catalyse substantial economic growth and significantly reduce the deficit.

While this estimate will not absolutely provide the full bouquet of required infrastructure, the investment will shift Nigeria from an infrastructure-deficient state to one with a rapidly modernised, connected, and sustainable system. Such investment could generate roughly 3 to 4 times as many jobs in the economy, significantly reducing unemployment and addressing the poor condition of road networks, enhancing air transport safety, and facilitating faster growth to support a modern digital economy, among other benefits.

*Historical Budget Allocation and the Possible Realisation of the $142bn Infrastructure Target*

Over the last 25 years, since 2000, no federal administration has budgeted more than $14 billion for capital spending in a single year, despite three oil booms between 2000 and 2014.

In 2000, for instance, total federal government projected capital expenditure was $3.62 billion, but only the first quarter was fully disbursed, with lower disbursements recorded in the second quarter to the last. Though the 2001 fiscal year was marked by high oil revenues and windfall gains (excess proceeds), the capital budget was $3.87 billion, but only the first-quarter allocation was fully disbursed.

In 2002, the total capital expenditure appropriated was $2.7 billion. Still, only about 38% of the capital budget was implemented, with appropriated capital expenditure declining to $2.25 billion in 2003 and recording a marginal increase to $2.6 billion in 2004.

Though capital spending increased to $ 4.6 billion in 2005, it was still a far cry from KPMG’s $14.2 billion suggested benchmark per annum, especially given that it marked the year of the oil windfall, when projected crude oil sales reached $37.7 billion. But only 55% of the budget was implemented by December, 2005. The trend of low capital appropriation continued in 2006, with total federal infrastructure spending cited at $4.5 billion.

In 2007, however, the capital budget ballooned to over $5 billion, propelled by an oil sale boom, but actual spending was about $3.9 billion. The same basic, relatively high capital budget appropriation was recorded in 2008, another oil price surge year, when about $6.7 billion was appropriated, with yet again a low implementation threshold. In 2009, approximately $7 billion was budgeted for capital expenditure, but only about 54.26% was released.

In tandem with the oil boom of 2010, 2011, 2012, and 2013, appropriated capital expenditure increased to about $12.3 billion, $10.42 billion, $8.2 billion, and $9.9 billion, respectively. However, all the appropriated expenditures were reported to have performed below 70 per cent.

We note that, beginning in 2014, after the global oil price upswing, capital expenditure returned to the $6 billion range. By 2015, however, earnings from crude oil had crashed, and that reflected in a reduced capital budget allocation of about $3.2 billion.

Nevertheless, as of September 2015, only about $1 billion had been spent on capital projects.

In 2016, there was a relative increase in both allocation and implementation, with about $3.95 billion released for capital projects. Paradoxically, the year of the oil crash recorded the highest capital release for infrastructure in the country’s history up to that point. The budget was successfully implemented through loans and related debts.

About $2 billion was specifically injected to revive abandoned projects in the year. In 2017, proposed capital expenditure was roughly $7.3 billion; however, about $4.5 billion was released. In 2018, capital expenditure was quite ambitious at about $9.42 billion, again with about $4.4 billion released. This was replicated in 2019 when total capital expenditure released was roughly $3.9 billion out of the approved capital budget of $6.6 billion. In 2020, budgeted capital expenditure was about $5.0 billion.

In 2021, planned capital expenditure totalled roughly $10.4 billion. However, the actual spending was about $5 billion. Beginning with the 2022 capital budget allocation, we observed an exponential increase in the capital budget to $13.34 billion; however, only about $4.29 billion was released. The value of capital expenditure declined to $9.3 billion in 2023, while actual performance was reported at $3.45 billion. Beginning in 2024, we observed a policy of rolling over outstanding appropriated expenditures into the following year to ensure their complete implementation. The 2024 capital expenditure was printed at about $13 billion, with a further increase to about $15 billion in the 2025 budget for restoration.

We note at this juncture the near-perennial low budget implementation threshold since 2000, with the obvious inconsequentiality of appropriated expenditure on infrastructural development.

However, at this time, we acknowledge the record-breaking fiscal milestone set by the President Tinubu-led federal administration, which matched and exceeded KPMG’s $14.2 billion annual infrastructure spending estimate for the first time in Nigeria’s fiscal history.

Based on the approved 2026 Appropriation Act, the Nigerian government significantly expanded its fiscal framework, with the total budget breaking records. Remarkably, the budget allocated $23 billion (roughly half the total budget) to infrastructure and other capital expenditures.

Without doubt, the 2026 budget is indicative of a new vista in the nation’s fiscal firmament with emphasis on securing debts for infrastructure development.

The approved $23 billion infrastructure budget is about the same size as the budget deficit to be financed almost entirely through debt.

This debt-for-infrastructure spending policy had roused a cacophony of concerns and, at times, condemnation in political opposition quarters and corporate advocacy groups. Some had orchestrated the fact that debts should not have been planned to finance the 2026 deficit since the removal of the fiscally ruinous fuel subsidy. The opposing argument is that the removal had saved the country about $10 billion, which should naturally revert to the federation account.

Our retort, however, is that the $10 billion annual fuel subsidy was mostly funded by debt and did not account for the bulk of the financing required for capital spending at that time or now. The country definitely needed more than the $10 billion saved from subsidies to provide functional infrastructural facilities.

Some other adversarial imputations have also argued that, rather than resorting to debt financing for infrastructure, the Public-Private Partnership (PPP) model should be vigorously adopted. We note, conversely, that several empirical studies have shown that PPPs in infrastructure financing face significant challenges, including high transaction costs, lengthy negotiation timelines, complex risk allocation, and political instability, which often result in projects being treated as off-balance-sheet liabilities.

Other key obstacles include limited institutional capacity to manage contracts, weak legal frameworks, insufficient financial resources and abandonment.

In addition, private investors are drawn more to jurisdictions that have demonstrated strong commitments to infrastructure investment because such commitments act as key indicators of economic stability, reduced operational risks, and enhanced profitability, unlike what obtains in Nigeria.

A substantive indicator of the private sector’s reluctance to enthusiastically embrace the infrastructure PPP in Nigeria is that institutional assets, including pension and insurance funds, have exceeded $100 billion, yet less than 5% is invested in infrastructure, compared to 15% in South Africa.

Private equity and venture capital flow to Nigeria reached $1.2 billion in 2023, but little of this was directed to infrastructure.

The reality is that manifest government funding of infrastructure assets usually motivates and builds investors’ confidence in the jurisdiction of interest.

Nonetheless, from both global and domestic indicators, there are growing signs of investors’ increased confidence in Nigeria’s debt instruments, evidenced by Nigeria’s sovereign Eurobonds yields, which fell last week to 6.89% from 8% for the first time on record. This signals improved sentiment among foreign portfolio investors towards the country and underscores the strength of demand for Nigeria’s external debt, even as global borrowing costs remain elevated.

This positive development is despite rising US Treasury yields, which usually attract investors away from emerging-market debt. Instead, investors are increasingly pricing in Nigeria’s improved macroeconomic stability, reform momentum and more recently, the rally in oil prices following the U.S.-Iran war. Thus, it can be safely asserted that the global capital market will provide Nigeria with a cheaper cost of debt in the future.

We also note that some Nigerian corporates express concerns about the crowding out of domestic companies from the debt market by the federal government’s borrowing there.

Our submission in this regard is that, at this point in the nation’s developmental trajectory, all considerations should be subject to the requirements of development infrastructure investment, with borrowed funds directed to high-priority projects in transportation, power, digital, healthcare, and education that enhance long-term productivity and economic growth.

We must add that the government’s issuance of domestic debt through bonds and treasury bills deepens local financial markets, helping to create a benchmark yield curve. This serves as a reference point for pricing private-sector debt and facilitates the growth of corporate bond markets.

*Conclusion*

Already, we are seeing clear signs of a rejuvenated Nigerian infrastructure, with the recent approval by the Tinubu-led Federal Executive Council of a record-breaking suite of infrastructure projects. These include $2.99 billion for rail projects in Lagos, Kano, and Kaduna, more than ₦7 trillion for road and bridge works nationwide, $billion worth of total reconstruction of major seaports in Apapa, Tin Can, Calabar, Warri, and Port Harcourt to address decades of neglect and ₦1.096 trillion for capital projects in the power sector, among others.

Omoniyi M. Akinsiju, PhD

Chairman,

Independent Media and Policy Initiative (IMPI)

May 17, 2026

{kind=link}